- March 2026 saw 45,000 tech layoffs alongside $131.5B in AI startup funding, signaling a reallocation within tech rather than a sector-wide downturn.

- AI and automation are increasingly cited as direct drivers of job cuts (9,200+ in March 2026; 55,000 in 2025), while AI investment grows sharply (+52% YoY) and non-AI funding declines (-10%).

- The article argues layoffs and AI funding are linked: capital is shifting away from labor-heavy knowledge-work models toward tools that automate or replace that labor.

- Displacement is role-specific, with routine maintenance, QA, content production, customer service, data processing, and mid-level coordination losing value as AI-native platforms and agent frameworks gain it.

- With 86% of enterprises increasing AI budgets and VCs betting on “the year of agents,” the pace of labor displacement is expected to accelerate.

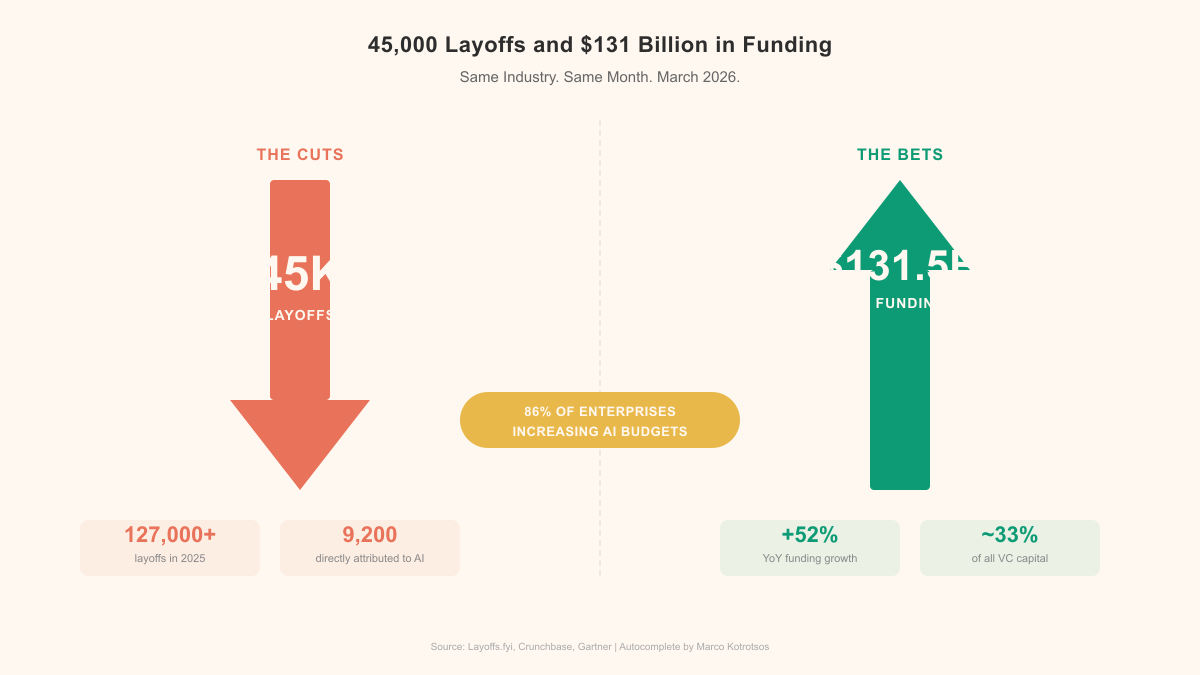

In March 2026, the technology industry laid off 45,000 workers. In that same period, AI startups attracted $131.5 billion in venture capital. Same industry. Same month. One side of the building is hiring movers to pack boxes while the other side is popping champagne over a Series B.

It's not a contradiction. It's a transfer. Capital is moving from one version of tech to another, and the people caught in the middle are finding out that their skills, their roles, their entire career trajectories were priced into the old version.

The numbers tell a single story

The layoff data is grim on its own. Over 127,000 workers were laid off at US tech companies in 2025, and 55,000 of those had AI cited explicitly as a contributing factor (Challenger, Gray & Christmas). March 2026 alone: 45,000 cuts, over 9,200 directly attributed to AI and automation.

Now look at the funding side. AI startup funding grew 52% year over year. Non-AI startups saw investment slip 10%. AI absorbs nearly one-third of all global venture capital.

| Metric | Value |

|---|---|

| Tech layoffs in March 2026 | 45,000 |

| Layoffs attributed to AI/automation | 9,200+ |

| US tech layoffs in 2025 (total) | 127,000+ |

| 2025 layoffs citing AI as factor | 55,000 |

| AI startup VC funding | $131.5 billion |

| AI funding growth (YoY) | +52% |

| Non-AI startup funding growth (YoY) | -10% |

| AI share of global venture capital | ~33% |

| Enterprises increasing AI budgets | 86% |

Put those columns next to each other and you're looking at a reallocation event. The money isn't leaving tech. It's leaving the humans in tech.

Capital doesn't care about your sprint velocity

There's a comforting narrative that says layoffs and funding surges are unrelated. Layoffs happen because of macro conditions, poor management, over-hiring during the pandemic. All partially true. None of it explains why the layoff-to-funding ratio has diverged so sharply along the AI fault line.

The divergence is directional. Investment in companies that employ lots of people to do knowledge work is declining. Investment in companies that build systems to replace that work is surging. Those aren't independent trends. They're two measurements of the same shift.

Investors aren't being subtle about it, either. Multiple VC firms have publicly predicted that 2026 will be "the year of agents," the year when AI systems start delivering measurable "human-labor displacement." Not speculation about some distant future. An investment thesis being executed right now, with $131.5 billion behind it.

86% of enterprises say they're increasing AI budgets. The question isn't whether displacement happens. It's how fast.

Who gets displaced, who gets funded

The pattern is specific enough to map. It's not "tech workers" versus "AI companies." It's a particular set of roles being drained of economic value while a different set accumulates it.

| Losing value | Gaining value |

|---|---|

| Routine software maintenance teams | AI-native development platforms |

| Large QA and testing departments | Automated testing and agent frameworks |

| Content production at scale | Generative content systems |

| Customer service headcount | AI-first customer interaction platforms |

| Data entry and processing teams | Automated data pipeline companies |

| Mid-level project coordination | AI workflow orchestration tools |

The people being laid off aren't incompetent. Many of them are excellent at jobs that are becoming economically indefensible. A team of twelve maintaining a legacy application can be replaced by three engineers with AI-augmented dev tools and an agent pipeline. The quality might even improve. Those twelve people didn't do anything wrong. Their economic equation just changed.

And that's what makes this moment particularly cruel. The layoffs aren't a judgment on the workers. They're capital chasing a different production model. The $131.5 billion isn't building better versions of existing companies. It's building replacements for the labor those companies used to rely on.

The year of agents, the year of displacement

The language investors use tells you everything. "The year of agents" is a polite way of saying "the year we automate human decision-making at scale." Agents aren't chatbots. They're autonomous systems that take actions, make choices, and complete workflows that previously required a person sitting in a chair, reading emails, attending meetings, exercising judgment.

Every dollar of that $131.5 billion is a bet that some category of human work can be done by software. Not assisted by software (that was the last decade). Done by software. That's this decade.

The companies receiving that funding are building systems designed to absorb the tasks that currently justify salaries. When investors say "human-labor displacement" in pitch meetings, they mean it literally. They're funding the construction of digital workers, and they expect returns in the form of companies needing fewer humans.

Not paranoia. The stated business model.

The gap in the middle

The most dangerous position right now is the middle. AI researchers and engineers building agent frameworks, training models, designing AI-native architectures, they've never been more in demand. Roles that require deep human interaction, physical presence, or genuinely novel problem-solving remain relatively insulated.

But the middle. The broad swath of knowledge workers who process information, coordinate activities, produce routine output, manage predictable workflows. That's where the floor is falling out. These are the 45,000. The 127,000. Competent professionals whose work happens to be the exact type of work that $131.5 billion is being deployed to automate.

Here's the part that stings: many of the people laid off this month will apply for jobs at the companies that were funded this month. Some will get hired. Most will find the new companies need a fraction of the headcount. That's the entire point of the investment.

What stays real

None of this means the technology industry is shrinking. By every financial measure, it's growing. Revenue up. Margins improving. Market caps climbing. The industry is healthier than it's been in years, if you measure by the metrics capital markets care about.

It just needs fewer people to generate that health.

That's how 45,000 layoffs and $131.5 billion in funding coexist. Not a contradiction. Not a coincidence. A transition from labor-intensive technology production to capital-intensive technology production. Money follows the model that scales without headcount. The headcount follows the money out the door.

The workers being displaced built the systems that made AI possible. They wrote the code, cleaned the data, managed the servers, shipped the products. The reward for that work is a job market that no longer values it at the same price. If that feels unfair, it's because it is. Capital doesn't optimize for fairness. It optimizes for returns, and right now, the returns are in replacing the people who built the foundation with systems that run on top of it.

That's not a future scenario. That's March 2026.

Assume the market is repricing roles, not just companies, and audit your work for tasks that can be automated versus decisions and ownership that can’t. If your job is heavy on routine execution (maintenance, QA, coordination, high-volume content or support), start shifting toward AI-augmented workflows, systems design, and domain-specific problem framing where you can supervise or integrate agents rather than compete with them. Watch where budgets are moving inside your org—AI tooling, automation, and data pipelines—and position yourself on the side that builds, governs, or operationalizes those systems.